Cg 20 10 07 04 Liability Endorsement PDF Form

The CG 20 10 07 04 Liability Endorsement form is an important document within the realm of commercial general liability insurance. It serves to add specific individuals or organizations as additional insured parties under an existing policy. This endorsement is particularly relevant for businesses that engage contractors or subcontractors, as it provides a layer of protection against claims related to bodily injury, property damage, or personal and advertising injury that may arise during ongoing operations. The form outlines essential details, including the names of the additional insured parties and the locations where the coverage applies. However, it is crucial to note that the coverage is limited to liabilities arising from the acts or omissions of the named insured or those acting on their behalf. Furthermore, the endorsement specifies that the insurance will not extend beyond what is mandated by any contract or agreement in place. Additional exclusions also apply, particularly concerning work that has been completed or when the project has been put to its intended use. The endorsement clarifies that the limits of insurance for additional insureds will not exceed the amounts required by contract or the available policy limits, ensuring that businesses remain compliant while managing risk effectively.

Common mistakes

-

Incomplete Information: Failing to provide all necessary details, such as the policy number or the names of additional insured persons or organizations, can lead to processing delays.

-

Incorrect Names: Misspelling the names of additional insured parties can result in coverage issues. Always double-check for accuracy.

-

Missing Locations: Not specifying the locations of covered operations may cause confusion and limit the effectiveness of the endorsement.

-

Ignoring Exclusions: Overlooking the specific exclusions listed in the endorsement can lead to misunderstandings about what is covered.

-

Not Understanding Limits: Failing to recognize the limits of insurance can result in unexpected liability exposure. Be sure to clarify the maximum coverage available.

-

Assuming Coverage: Assuming that coverage is automatically granted without a contract or agreement may lead to gaps in protection. Always confirm the requirements.

-

Late Submission: Submitting the form after the required deadline can invalidate the endorsement. Timeliness is crucial for effective coverage.

Example - Cg 20 10 07 04 Liability Endorsement Form

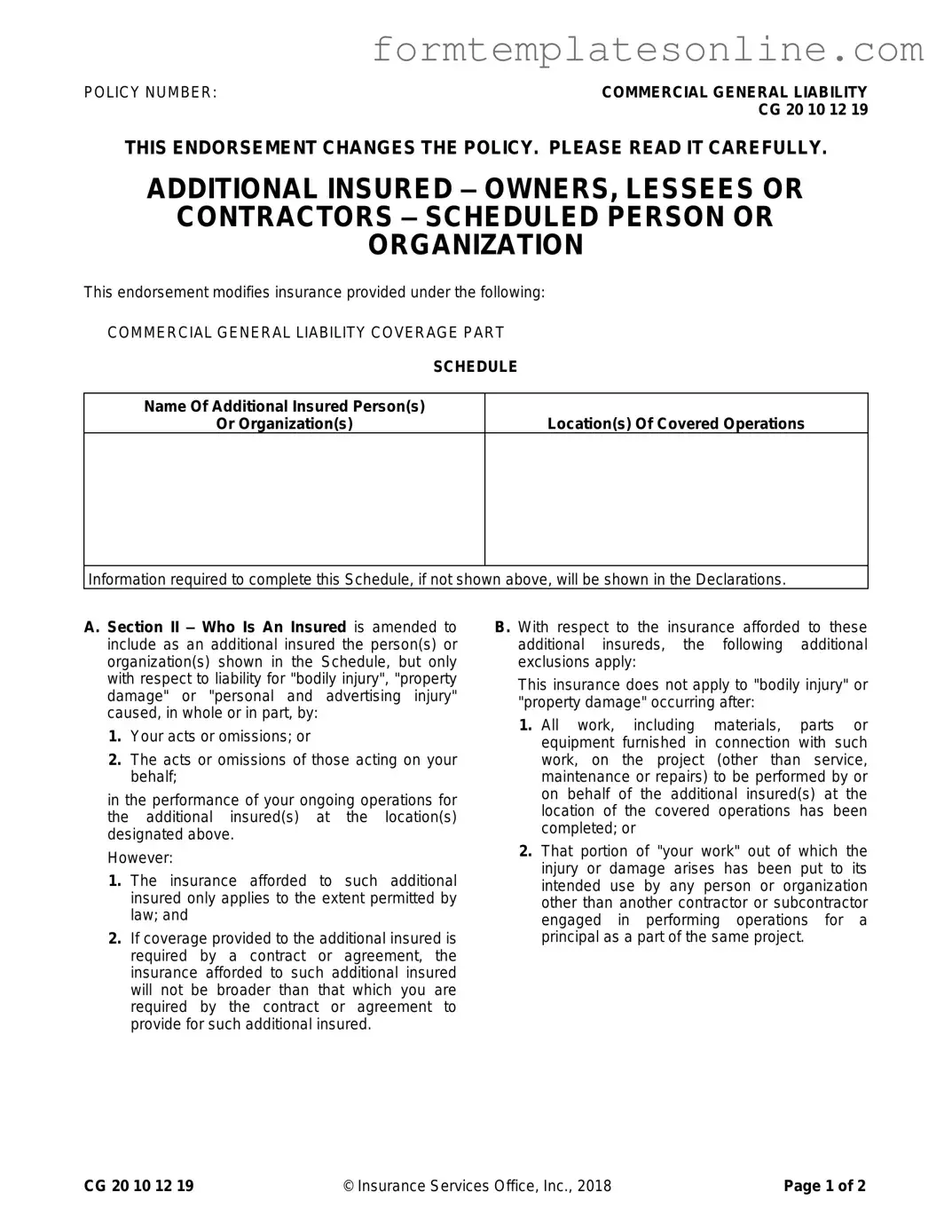

POLICY NUMBER: |

COMMERCIAL GENERAL LIABILITY |

|

CG 20 10 12 19 |

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY.

ADDITIONAL INSURED – OWNERS, LESSEES OR

CONTRACTORS – SCHEDULED PERSON OR

ORGANIZATION

This endorsement modifies insurance provided under the following:

COMMERCIAL GENERAL LIABILITY COVERAGE PART

SCHEDULE

Name Of Additional Insured Person(s)

Or Organization(s)

Location(s) Of Covered Operations

Information required to complete this Schedule, if not shown above, will be shown in the Declarations.

A. Section II – Who Is An Insured is amended to include as an additional insured the person(s) or organization(s) shown in the Schedule, but only with respect to liability for "bodily injury", "property damage" or "personal and advertising injury" caused, in whole or in part, by:

1.Your acts or omissions; or

2.The acts or omissions of those acting on your behalf;

in the performance of your ongoing operations for the additional insured(s) at the location(s) designated above.

However:

1.The insurance afforded to such additional insured only applies to the extent permitted by law; and

2.If coverage provided to the additional insured is required by a contract or agreement, the insurance afforded to such additional insured will not be broader than that which you are required by the contract or agreement to provide for such additional insured.

B. With respect to the insurance afforded to these additional insureds, the following additional exclusions apply:

This insurance does not apply to "bodily injury" or "property damage" occurring after:

1.All work, including materials, parts or equipment furnished in connection with such work, on the project (other than service, maintenance or repairs) to be performed by or on behalf of the additional insured(s) at the location of the covered operations has been completed; or

2.That portion of "your work" out of which the injury or damage arises has been put to its intended use by any person or organization other than another contractor or subcontractor engaged in performing operations for a principal as a part of the same project.

CG 20 10 12 19 |

© Insurance Services Office, Inc., 2018 |

Page 1 of 2 |

C. With respect to the insurance afforded to these additional insureds, the following is added to

Section III – Limits Of Insurance:

If coverage provided to the additional insured is required by a contract or agreement, the most we will pay on behalf of the additional insured is the amount of insurance:

1.Required by the contract or agreement; or

2.Available under the applicable limits of insurance;

whichever is less.

This endorsement shall not increase the applicable limits of insurance.

Page 2 of 2 |

© Insurance Services Office, Inc., 2018 |

CG 20 10 12 19 |

More About Cg 20 10 07 04 Liability Endorsement

What is the purpose of the CG 20 10 07 04 Liability Endorsement form?

The CG 20 10 07 04 Liability Endorsement form serves to add additional insured parties to a commercial general liability policy. This endorsement specifically extends coverage to owners, lessees, or contractors who are named in the endorsement schedule. It is designed to protect these additional insureds from liabilities arising from bodily injury, property damage, or personal and advertising injury linked to the insured's operations.

Who qualifies as an additional insured under this endorsement?

Individuals or organizations listed in the endorsement schedule qualify as additional insureds. The endorsement applies to them only in relation to liabilities that arise from the acts or omissions of the primary insured or those acting on their behalf during ongoing operations at designated locations. This ensures that the additional insureds have coverage for specific risks associated with the insured's work.

What are the limitations of coverage for additional insureds?

Coverage for additional insureds is subject to specific limitations. It only applies to the extent permitted by law, and if required by a contract, the coverage cannot exceed what the primary insured is obligated to provide. Additionally, coverage does not extend to bodily injury or property damage that occurs after the completion of all work on the project, unless it relates to service, maintenance, or repairs.

How does the endorsement affect the limits of insurance?

The endorsement does not increase the applicable limits of insurance. If coverage is required by a contract, the maximum amount payable on behalf of the additional insured is the lesser of the required contract amount or the available limits under the primary insured’s policy. This ensures that the financial exposure remains within the originally established limits.

What exclusions apply to the coverage provided for additional insureds?

Several exclusions apply to the coverage for additional insureds. Notably, coverage does not apply to bodily injury or property damage that occurs after the completion of work related to the project, except for ongoing service or maintenance. Additionally, if the injury or damage arises after the work has been put to its intended use by someone other than another contractor or subcontractor, coverage will not apply.

How should the schedule for additional insureds be completed?

The schedule must list the names of the additional insured persons or organizations and the locations of the covered operations. If this information is not included in the endorsement itself, it will be documented in the policy declarations. Accurate completion of this schedule is essential for ensuring proper coverage for all parties involved.

Is it necessary to read the endorsement carefully?

Yes, it is crucial to read the CG 20 10 07 04 Liability Endorsement form carefully. The endorsement modifies the underlying policy and contains important information regarding coverage, limitations, and exclusions. Understanding these details helps ensure that all parties are aware of their rights and responsibilities under the insurance policy.

Key takeaways

When filling out and using the CG 20 10 07 04 Liability Endorsement form, consider the following key takeaways:

- Policy Number: Always include the correct policy number, which is crucial for identifying the insurance coverage.

- Additional Insureds: Clearly list the names of the additional insured persons or organizations in the designated section.

- Location of Operations: Specify the locations where the covered operations will take place to ensure proper coverage.

- Coverage Scope: Understand that the endorsement modifies the existing policy to include additional insureds only for specific liabilities.

- Acts or Omissions: The coverage applies to liabilities arising from your acts or those acting on your behalf during ongoing operations.

- Legal Limitations: The insurance coverage is subject to the limits permitted by law, which may affect the extent of coverage.

- Contractual Requirements: If a contract requires coverage for additional insureds, ensure that the insurance provided does not exceed what is specified in that contract.

- Exclusions: Be aware of exclusions that apply, particularly regarding injuries or damages occurring after project completion.

- Limit of Insurance: The maximum amount payable on behalf of the additional insured is the lesser of the contract requirement or the available limits.

- No Increase in Limits: The endorsement does not increase the overall limits of the insurance policy, so plan accordingly.

By keeping these points in mind, you can effectively navigate the process of filling out and utilizing the CG 20 10 07 04 Liability Endorsement form.

Form Attributes

| Fact Name | Description |

|---|---|

| Purpose of Endorsement | This endorsement adds additional insured status for owners, lessees, or contractors to a commercial general liability policy. |

| Coverage Limitations | The coverage for additional insureds is limited to liability arising from the named insured's acts or omissions during ongoing operations. |

| Exclusions | Liability for bodily injury or property damage is excluded once the work at the project location is completed or when the work is put to its intended use. |

| Contractual Requirements | The coverage provided cannot exceed what is required by any contract or agreement with the additional insured. |

Other PDF Forms

Odometer Disclosure Texas - Failure to provide an accurate odometer reading can result in fines.

The Dirt Bike Bill of Sale form is a crucial document used when buying or selling a dirt bike in New York. This form serves to record the transaction, providing both parties with proof of ownership and details about the sale. For more information and to access a template, you can visit documentonline.org/blank-new-york-dirt-bike-bill-of-sale/. Understanding its importance can help ensure a smooth and legal transfer of ownership.

Puppy Health Record - Monitor your puppy’s fluctuating weight as it progresses through growth stages.

Dos and Don'ts

When filling out the CG 20 10 07 04 Liability Endorsement form, keep the following tips in mind:

- Do ensure that all required information is accurately completed, including the name of the additional insured and the location of covered operations.

- Do read the entire endorsement carefully to understand how it modifies your insurance policy.

- Don't leave any sections blank; incomplete forms can lead to delays or issues with coverage.

- Don't assume that the coverage is automatic; verify that it aligns with any contractual obligations you may have.